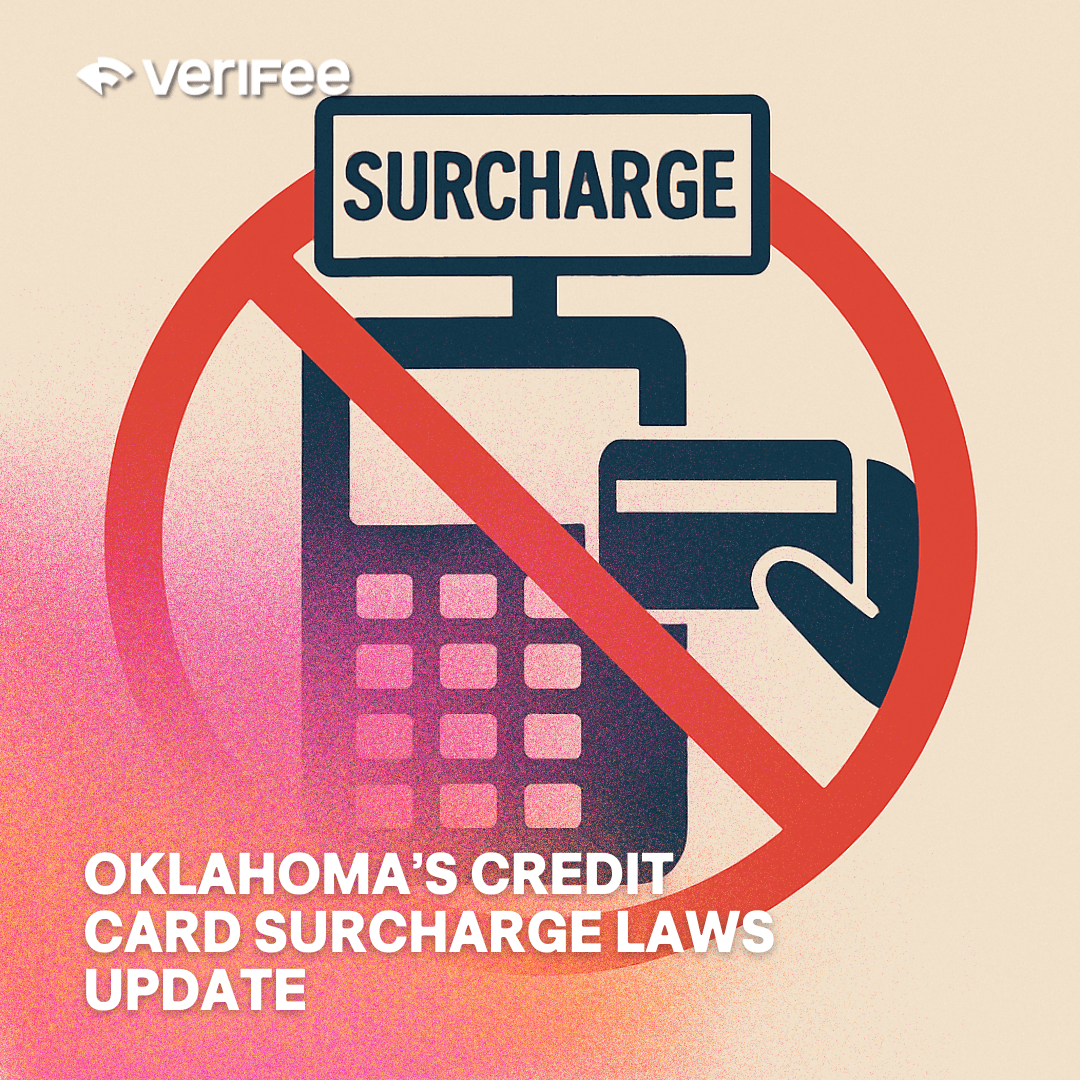

Effective November 1, 2025, Oklahoma will allow credit card surcharges under strict rules: only on credit cards, capped at 2%, and with clear disclosures. But even with these limits, merchants won’t recover full costs—especially on high-fee cards like Amex—and debit surcharges remain illegal. VeriFee recommends cost reduction over surcharging through its Blended Inclusive Pricing, helping businesses lower fees without burdening customers.

Global Payments’ $24B WorldPay Power Play

Worldpay just got sold… again… After bouncing from FIS to GTCR, it’s now Global Payments’ $24B prize. But this isn’t innovation; it’s consolidation with a potential side of chaos. Merchants brace for tech glitches, service breakdowns, and pricing “synergies.” Is this Worldpay’s fresh start or a fresh acquisition hangover? Embedded payment partners, beware: you’re on this rollercoaster too. This deal could reshape the industry, or break it.

Read more

Chargebacks Are Skyrocketing – How Merchants Can Slash Costs & Risks

Chargebacks are surging, with global disputes expected to hit 324 million by 2028 and costs rising to $41.7B. Drivers include card-not-present fraud, subscription confusion, friendly fraud, and easier dispute filing. The true cost of a chargeback far exceeds the refund, including fees, labor, and lost goods. To reduce impact, merchants must adopt automation, real-time alerts, data-driven fraud tools, and streamlined processes. Chargebacks are now a major business risk requiring strategic focus.

Read more

Interchange Inequality: You Thought Interchange Was Standard? Think Again.

Not all “interchange” is created equal. While it sounds like a standard fee, processors often manipulate the term—bundling in hidden markups, junk fees, and vague categories. There’s no industry-wide definition or standard, making true comparisons nearly impossible without a technical review. What looks like apples-to-apples rarely is. Surface-level rates can be deeply misleading without expert analysis.

Read more

Reimagining Non-Dues Revenue

Associations can rethink non-dues revenue by focusing on member savings instead of additional fees or programs. One major opportunity lies in helping members reduce hidden costs—like excessive payment processing fees—turning financial advocacy into a sustainable, high-impact revenue stream that boosts retention, adds value, and reinforces the association’s role as a true ally.

Read more

The Hidden EBITDA Lever

Elite investors are boosting valuations by targeting overlooked payment processing fees. VeriFee helps portfolio companies unlock 0.5% in revenue savings—translating to millions in EBITDA without operational changes. In a tough M&A landscape, this “frictionless optimization” delivers instant ROI. With no disruption, upfront cost, or vendor switch, it’s the clearest lever for IRR improvement, exit amplification, and roll-up advantage.

Read more

stay enlightened

Get the clear, simple information you deserve.